U nas zapłacisz kartą

U nas zapłacisz kartą

Przedłużanie włosów - Sposoby, Koszty i Porady dla Perfekcyjnego Efektu

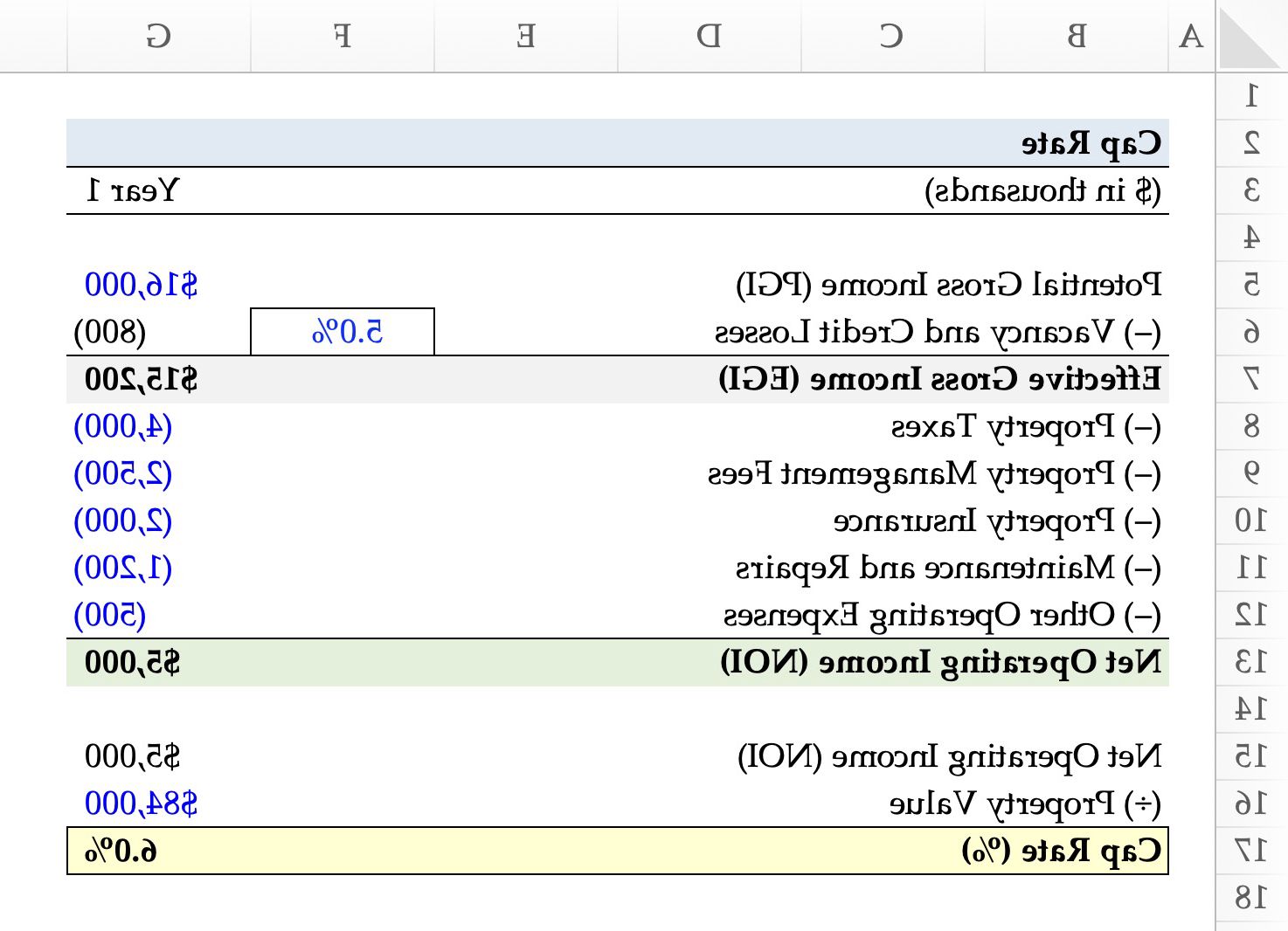

How to Model For Cap Ex

As a result of modeling this way, cap ex is not considered when deriving a purchase price based on a cap rate (NOI/Cap Rate = Value). Does this pose a problem for potential investors if they are excluding potentially significant expenses from their formula to derive a purchase price?

Not really. As long as the investor is taking a holistic approach to the valuation and is including the capital expenditures when looking at return metrics such as the IRR and Equity Multiple, then the investor should be clear eyed about the opportunity. If there is a significant amount of cap ex needed that reduces returns, then an investor can adjust their going in cap rate up (higher cap rate equals lower purchase price) accordingly in order to meet their return objectives.

Capital Reserves

One nuance to underwriting cap ex is capital reserves. It is common practice to include an annual capital reserve allocation that will be funds set aside from the operating cash flow for future capital improvements. Does a known and reoccurring capital reserve amount that is budgeted for and being deducted from the asset’s cash flow become a part of the op ex?

For office, retail, and industrial, capital reserves are usually modeled below the NOI.

Is a Higher Cap Rate Better?

The cap rate is a measure of returns, so the metric is also a measure of risk since risk and return are two sides of the same coin.

In short, the answer is rather nuanced and subject to the specific investment strategy, minimum required rate of return, and risk tolerance specific to the investor.

However, the notion that all real estate investors prefer a higher cap rate is misinformed.

Why? Certain real estate investors prioritize capital preservation—minimizing the risk of capital loss on an investment—whereas others are more yield-oriented and set a higher bar for the required rate of return.

- Higher Cap Rate ➝ Real estate properties with higher cap rates are perceived as riskier investments with less stability in their cash flow. However, the increased riskiness of the cash flows can be appealing to certain yield-oriented commercial real estate (CRE) investors, as the potential upside is greater.

- Lower Cap Rate ➝ On the other hand, real estate properties with lower capitalization rates are viewed as more conservative investments that generate stable income. Thus, risk-averse commercial real estate (CRE) investors are likely to find properties with steady income and situated in low-growth markets to be more attractive.

The trade-off here is that the predictability of the property’s NOI reduces the potential to earn an outsized yield above the original projection, barring unforeseen circumstances.

The risk tolerance varies by the specific investor, which goes hand-in-hand with the prior factor, as undertaking incremental risk must be compensated with a higher return.

Cap Rate vs. Cash on Cash Return: What is the Difference?

The difference between the cap rate and cash yield is as follows:

- Cap Rate ➝ The cap rate is the return expected on a rental property investment. Unlike the cash yield, the cap rate neglects the effects of financing (i.e. capital structure neutral) since the numerator is net operating income (NOI), an unlevered profitability metric unaffected by discretionary financing decisions. Therefore, the cap rate excludes financing costs such as interest and mortgage payments.

- Cash Yield ➝ The cash yield, or “cash on cash return,” is the annual pre-tax levered cash flow received per dollar of equity invested. In contrast to the cap rate, the cash yield is a levered metric (post-financing) because the debt service reduces the annual pre-tax cash flow.

The formula to calculate the cash yield consists of dividing the levered cash flow of a property by the equity investment contributed by the real estate investor.

Cash Yield (%) = Levered Cash Flow ÷ Equity ContributionThe levered cash flow is the rental income a property generates after deducting the annual debt service but before income taxes. The equity contribution is the cash investment (or “down payment”) the investor needs to close the real estate transaction.

The cap rate is a pro-forma measure of the implied return on an investment property as of the date of acquisition. In contrast, the constant denominator in the cash yield remains indifferent to the current state of the real estate market conditions, considering fixed purchase price and equity contribution.

The cash yield can determine the return earned on an equity investment on a rolling basis, where the percentage return fluctuates over time in tandem with the cash flow generated.

Since net operating income (NOI) neglects the effects of debt financing, the cap rate is better suited for comparative analysis, unlike the cash-on-cash return.

Cap Rate Example

Suppose a commercial rental property is expected to generate $12 million in net operating income (NOI) in 2024, and comparable properties nearby are trading at a 6.0% market cap rate.

The 6% market cap rate reflects the annual percentage return on investment (ROI) on the rental property, assuming the property was purchased outright without financing.

The direct capitalization method, one of the core real estate appraisal techniques, states the value of a property can be estimated by dividing its stabilized NOI by the market cap rate.

Implied Property Value = Stabilized NOI ÷ Market Cap RateGiven the 6.0% market cap rate, the implied market value of the property is $200 million.

- Implied Property Value = $12 million ÷ 6.0% = $200 million

Since net operating income (NOI) and property value—the two variables in the cap rate formula—are known, we can solve for the cap rate by dividing the NOI by the property value.